Vegetable oil prices ease as Middle East tensions subside

1 RM (Malaysian Ringgit) = 0.25 USD

1 USD = 0.75 GBP

*Exchange rates calculated and market prices reported on July 3, 2026

Crude Palm Oil

Average World Bank June 2026 palm oil price

US$1,105/tonne (-US$31 during the month, a decrease of 2.7%)

Malaysia palm market

Malaysia palm market

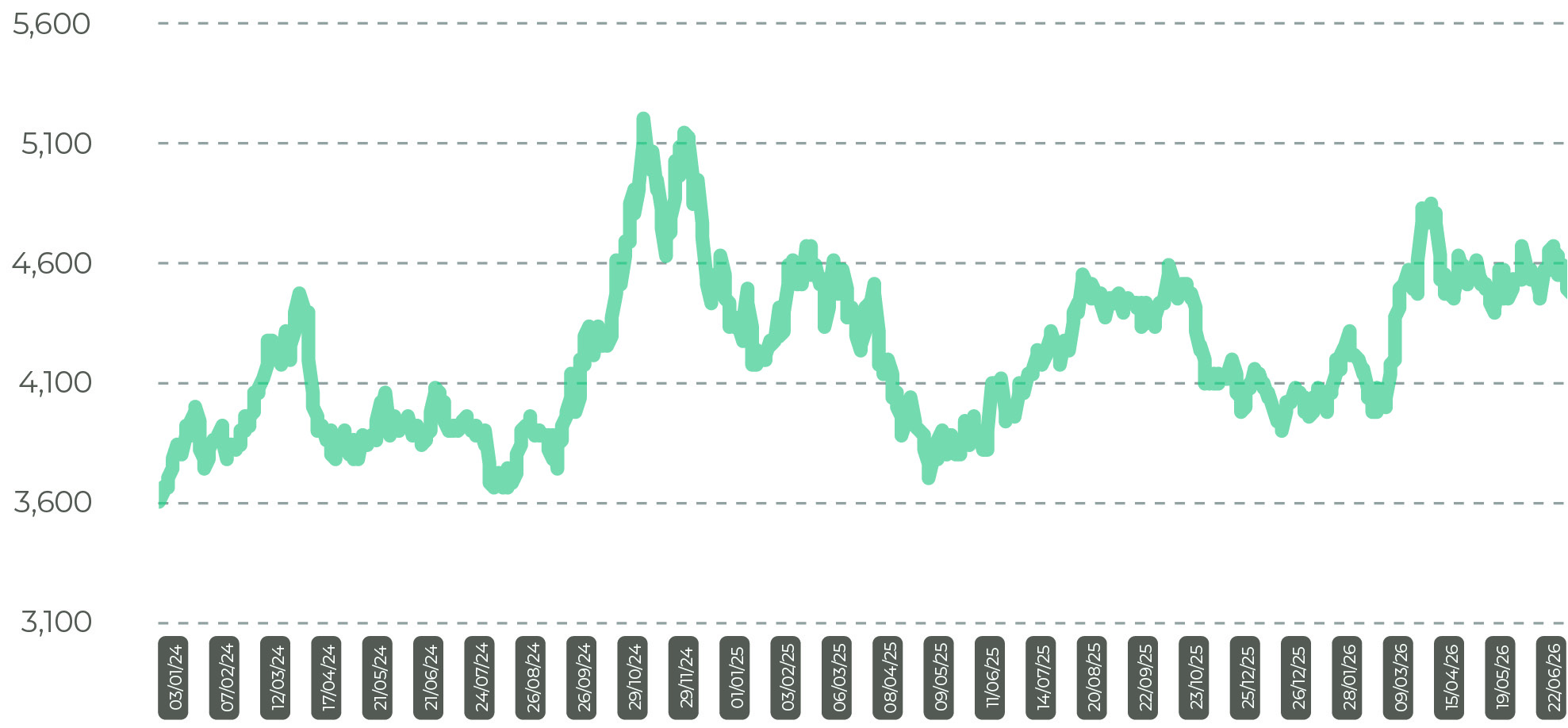

Palm oil prices fluctuate, but trend remains downward

Malaysian palm oil prices have fluctuated over the past month in response to changes in crude oil prices following an agreement between the U.S. and Iran to end hostilities in the Middle East.

On July 3, the average Malaysian palm oil settlement price on the Malaysian exchange was RM4,483/tonne (US$1,121), a drop of 4.1% during the month and the lowest price since 26 May 2026. The value was still 5.3% higher than just before the start of the conflict in late February. Compared with a year earlier, the price was 9.1% higher and 36.9% below the all-time high recorded in April 2022.

Malaysia CPO Settlement Price RM

Vegetable oil

Other vegetable oil prices also decline

There was downward pressure on crude oil and most vegetable oil prices in June as conflict eased in the Middle East. The average crude oil price fell 18.6% during the month to US$82 per barrel, according to the World Bank. That was 18.2% higher than the price a year earlier.

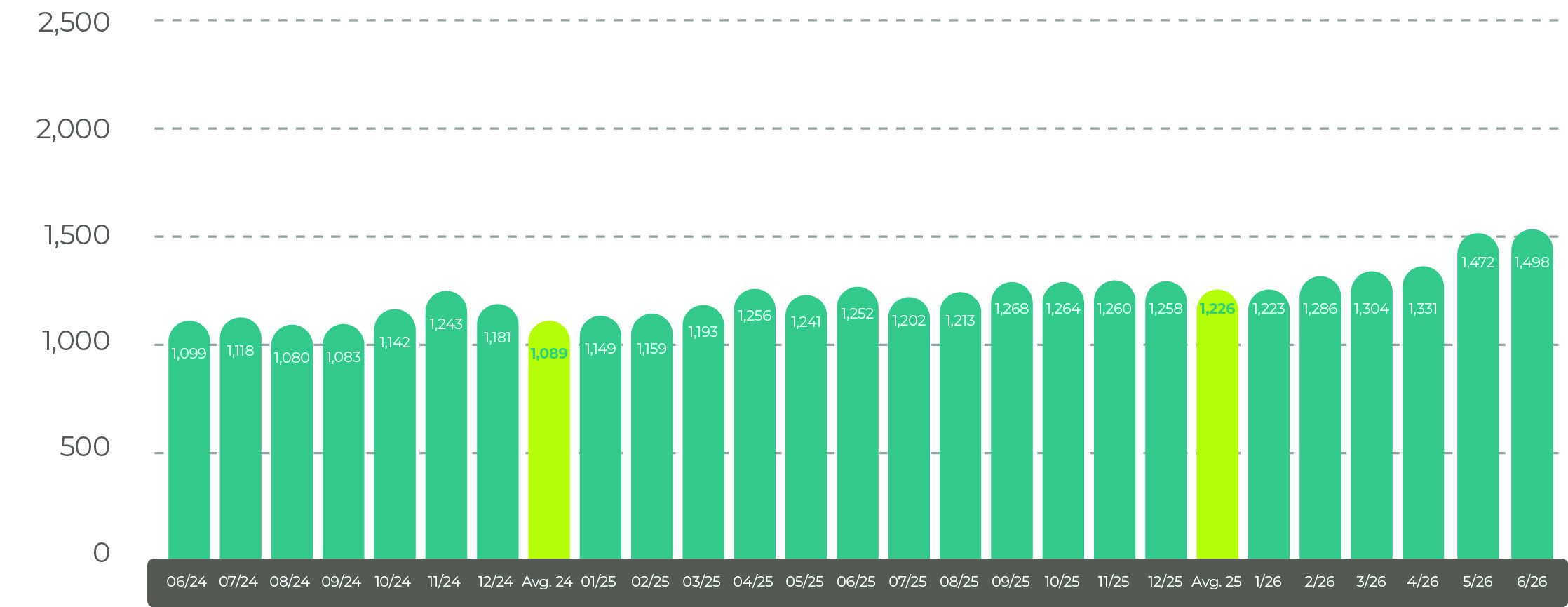

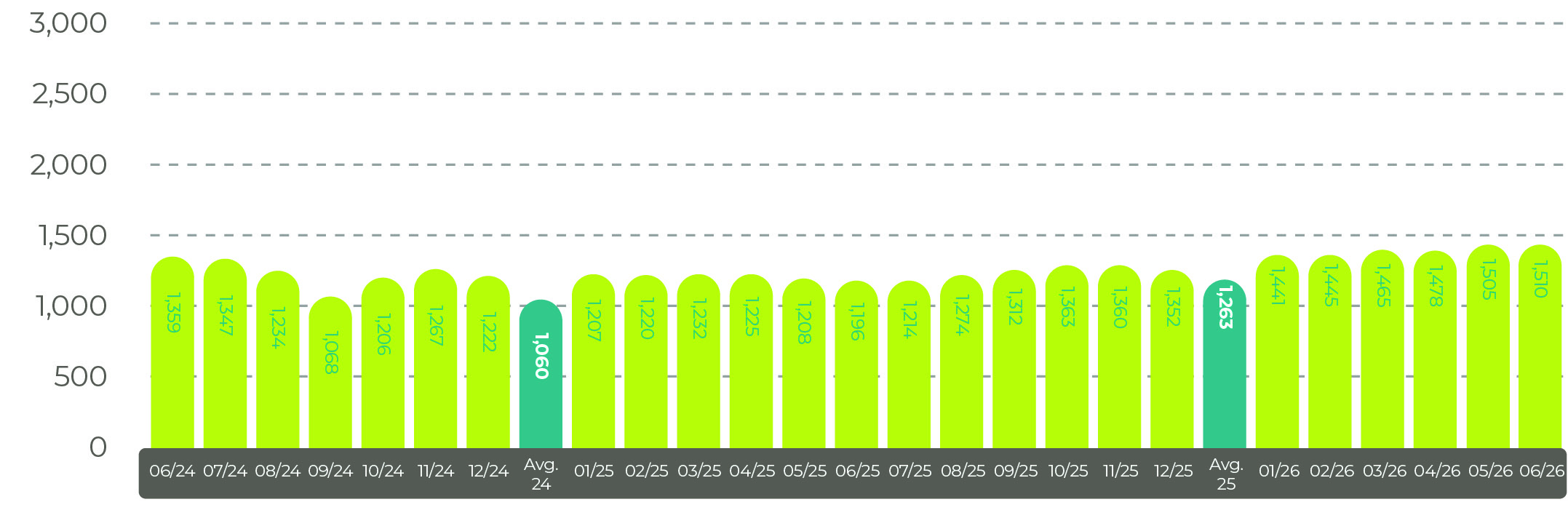

Global palm oil prices fell 2.7% during the month to US$1,105/tonne, which was 18.2% higher than in June 2025. Soybean oil prices were 0.9% lower during the month at US$1,765/tonne, an increase of 50% compared with June 2025. Rapeseed and sunflower oil bucked the downward trend, with rapeseed oil rising 0.7% during the month and 19.6% over the year to US$1,498/tonne. Sunflower oil increased 0.5% in June compared with May and was 26.3% higher than in June last year.

Global oilseed markets were relatively stable in June, according to the U.S. Department of Agriculture. Total production for 2026-27 was unchanged, as increased Russian sunflower seed output offset lower Russian soybean production. Trade was also unchanged, with higher Argentine soybean exports balancing reduced Russian exports. Global crushing remained stable, while carryout stocks increased because of larger sunflower seed stocks in Russia and soybean stocks in Argentina, partly offset by lower European Union rapeseed stocks.

The estimated U.S. 2026-27 average soybean price remained at US$11.40 per bushel, which was 9.6% higher than the 2025-26 season

Global vegetable oil stocks stood at 244.1 million tonnes in June, according to the U.S. Department of Agriculture, unchanged from May but 2.6% higher than in June 2025. Trade was estimated to be 3.6% higher than a year earlier at 91.8 million tonnes, with usage 2.8% higher at 237.6 million tonnes, while stocks were 0.7% higher at 30.4 million tonnes.

Average world soybean oil prices in US$/tonne

Rapeseed oil

Average world rapeseed oil price in US$/tonne

Sunflower oil

Average world sunflower oil prices in US$/tonne

Shipping update

Shipping costs jump by almost two-thirds in a month

Despite the agreement between the U.S. and Iran to allow freer movement of ships through the Strait of Hormuz, the Drewry World Container Index continues to climb and is now at its highest level in more than a year.

The latest price on July 2 was US$4,530 per 40-foot container, which was 8.8% higher than the previous week, 61.8% higher than a month earlier and 51.8% higher than a year earlier. Shipping costs measured by the index have increased by 175% since last October and have risen by 138% since the beginning of the Middle East conflict.

From the July 2, 2026 Drewry World Container Index report:

- The Drewry World Container Index (WCI), the benchmark widely referenced by procurement teams, surged 9% to US$4,530 per 40-foot container because of rate increases on the Trans-Pacific and Asia-Europe trade routes.

- On the Trans-Pacific trade route, spot rates continued to strengthen, with those from Shanghai to New York rising 11% to US$7,902 per 40-foot container and Shanghai to Los Angeles increasing 10% to US$6,349 per 40-foot container. According to Drewry's Container Capacity Insight, eight blank sailings have been announced on the Trans-Pacific trade route for next week, reflecting tight capacity. Carriers continue to announce General Rate Increases (GRIs) and Peak Season Surcharges (PSS) for July in anticipation of strong cargo volumes, with HMM introducing a Peak Season Surcharge of US$3,000 per 40-foot container, effective 15 July. Drewry expects rates to rise further in the coming weeks.

- On the Asia-Europe trade route, spot rates increased this week as carriers implemented higher Freight All Kinds (FAK) rates and Peak Season Surcharges amid strong peak-season demand. Freight rates from Shanghai to Genoa rose 10% to US$6,360 per 40-foot container, while rates from Shanghai to Rotterdam increased 7% to US$4,682 per 40-foot container. According to Drewry's Container Capacity Insight, only one blank sailing has been announced on the Asia-Europe trade route for next week as carriers maintain disciplined capacity management amid strong demand. Drewry expects rates to continue rising in the coming weeks.

- The east-west container freight market has remained resilient this year, supported by early peak-season demand and higher shipping costs resulting from geopolitical disruptions. The interim U.S.-Iran agreement has facilitated the reopening of the Strait of Hormuz, with vessel traffic recovering following the evacuation of stranded ships and the designation of authorised transit routes. However, security risks remain elevated following the suspension of ship escort operations after an attack on a containership near Oman. As a result, ongoing geopolitical tensions in the Middle East continue to underpin market uncertainty.

Source: Drewry Supply Chain Advisors

Disclaimer: The information in this document has been obtained from or based upon sources believed to be reliable and accurate at the time of writing. The document should be for information purposes only and is not guaranteed to be accurate or complete.